Cloud security in banking: Market trends and opportunities

May 29, 2026 13 min read 231 views

Banks are spending record sums to secure the cloud environments that now run their payments. According to a report by Allied Market Research, the cloud banking market is projected to reach $301 billion by 2032, growing at 16.3% annually. And yet the arrival of frontier AI models capable of finding and weaponizing software vulnerabilities in hours rather than months has compressed the timetable on which bank security has traditionally operated. What follows is a look at where cloud security in the banking industry stands now, what a Claude Mythos disclosure has changed about new threats, and what the better-prepared institutions are doing in response.

A meeting at the Treasury

When Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell summoned the chief executives of America’s largest banks to an unannounced meeting, the subject was not interest rates or a wobbling regional lender. It was a piece of software.

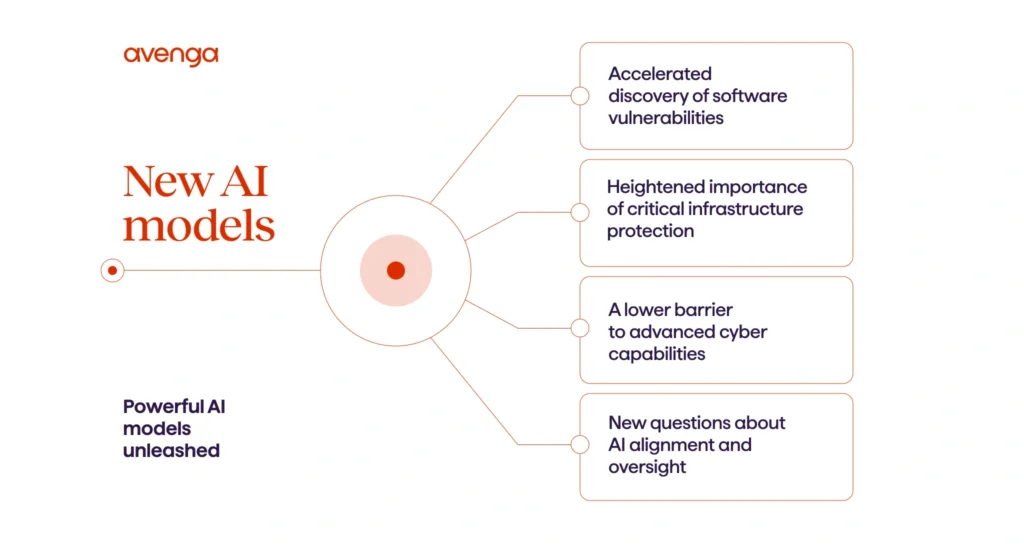

The software in question, an Anthropic model code-named Claude Mythos, had quietly uncovered thousands of severe vulnerabilities in operating systems, browsers, and enterprise platforms, including a 27-year-old flaw buried inside OpenBSD. Anthropic withheld the model from public release, distributing it through a restricted program called Project Glasswing. The Treasury briefed bank chiefs because their institutions were, in the dry phrasing of one regulator, “uniquely exposed.”

The episode crystallized something the financial industry has spent the better part of a decade trying not to acknowledge out loud. The cloud platforms that now run the world’s payments, trading desks, and customer ledgers have become, simultaneously, the engines of modernization and the largest single attack surface in banking history. The economic case for cloud services was always overwhelming. The security case has always been complicated. And the arrival of frontier AI is complicating it further.

Main threats to banking cloud security

The number of threats facing a modern bank cloud is longer than it was five years ago, and the items on it interact in ways that older threat models did not anticipate. A useful way to analyze this landscape is to group the dangers by where, in the stack, they originate.

AI-driven attacks

Generative and Agentic AI have changed the economics of cyberattacks. Capabilities that once required nation-state resources are now up for grabs. Convincing voice clones of executives, polymorphic malware, and real-time social engineering can all be produced at scale.

For banks, this manifests in three ways. AI-powered botnets are extending the duration and complexity of distributed denial-of-service campaigns. Attackers are also beginning to target the AI systems banks deploy internally, with techniques such as data poisoning, model manipulation, and prompt injection.

The third shift is the rise of autonomous attack agents. These systems can plan, adapt, and execute an entire attack lifecycle with minimal human direction. Banks that lack AI-aware detection, behavioral analytics, and model governance will find legacy fraud tools increasingly outmatched.

Identity and access management (IAM) failures

Identity has replaced the network perimeter as the principal control plane in cloud banking. Weaknesses in IAM now translate directly into a risk of data breach. The vast majority of breaches involve compromised or misused privileged credentials.

The problem is amplified by the explosion of non-human identities. Service accounts, API keys, machine tokens, and workload identities now far outnumber human users. Many carry excessive privileges and weak rotation policies, making cloud identity governance a defining discipline of modern banking security.

Common failure patterns are well known. Orphaned accounts remain active after staff or contractors leave. SMS-based MFA is bypassed through SIM-swapping or proxy phishing kits. Third-party vendor portals run on reused or default credentials. Standing privileged access violates least-privilege principles.

The remediation roadmap is established: phishing-resistant authentication, just-in-time privilege elevation, identity threat detection and response, and automated joiner-mover-leaver workflows. Adoption across the sector, however, remains uneven.

Insider threats

Insider risk in banking is structurally different from other industries. The data is valuable, the regulatory consequences of misuse are severe, and the workforce itself is under financial pressure. Most privilege misuse cases are financially motivated.

Three insider categories require distinct controls. Malicious insiders exploit legitimate access to exfiltrate sensitive data or manipulate transactions. Negligent insiders cause incidents through misconfigured shares, mishandled credentials, or unauthorized use of generative AI tools that leak data into third-party models.

Compromised insiders are in the third category. These are legitimate employees whose accounts have been taken over by external actors, often via business email compromise or session-token theft. IT administrators and other privileged users represent the highest-risk group.

User and entity behavior analytics, cloud-aware data loss prevention, and privileged access management with session recording are now baseline requirements rather than mature-state aspirations.

Misconfiguration of cloud resources

Misconfiguration remains the most common and most preventable cause of cloud breaches in banking. The shared responsibility model places configuration squarely on the customer. Many institutions still treat cloud security as an extension of legacy data center practices.

The most consequential misconfigurations are recurring. Object storage containers are left publicly exposed. IAM roles grant wildcard privileges to compute workloads. Databases and backups remain unencrypted. Logging is disabled, defeating forensic reconstruction. Security groups are opened during maintenance and never reverted.

The challenge scales nonlinearly with cloud adoption. A multi-cloud bank may operate tens of thousands of resources across its cloud infrastructure, with configurations drifting continuously through automated deployments.

Cloud Security Posture Management and Cloud-Native Application Protection Platforms are now the standard response. They work best when paired with policy-as-code guardrails embedded directly into CI/CD pipelines, so misconfigurations are blocked before deployment rather than detected after exposure.

API and application vulnerabilities

The API layer has become the defining attack surface of modern banking. Open banking mandates, real-time payment rails, embedded finance partnerships, and mobile-first digital banking experiences have multiplied exposed endpoints by an order of magnitude. Attackers have noticed, and the banking sector now reports the highest rate of API-related security incidents in any industry.

The vulnerability profile is broad. Broken object-level authorization allows horizontal access to other customers’ accounts. Excessive data exposure leaks sensitive fields in API responses. Weak rate limiting enables credential stuffing and enumeration.

Undocumented “shadow” and “zombie” APIs fall outside security inventories entirely. Business logic flaws unique to banking services evade automated scanners. Advanced bots compound the threat by mimicking human behavior at scale.

Enterprise-grade API security requires a layered approach: continuous API discovery, schema-aware traffic inspection, behavioral anomaly detection, dedicated bot management, and shift-left security testing integrated into development.

Ransomware and destructive malware

Ransomware has evolved from a disruptive nuisance into an existential operational risk. Financial services consistently rank among the hardest-hit sectors. The majority of institutions have experienced at least one ransomware incident in recent years.

The business model is now double or triple extortion. Attackers exfiltrate financial data before encryption, then threaten public release or regulatory notification. This neutralizes backup-only recovery strategies.

Targeting has become more surgical. Ransomware groups increasingly focus on critical systems such as payment gateways, core banking platforms, and customer databases, where operational disruption maximizes leverage.

Entry vectors have also moved into the cloud. Compromised SaaS administrator credentials, exposed cloud storage, and CI/CD pipeline takeovers now rival traditional phishing as initial access points.

Resilience strategies must extend beyond endpoint detection. Immutable and air-gapped backups for cloud workloads, micro-segmentation between core banking and corporate networks, and validated recovery procedures with defined RPO and RTO targets are essential. Tabletop exercises should include legal, communications, and regulatory dimensions of a destructive attack.

Best practices for ensuring cloud security in banking

Defending a modern banking cloud estate is no longer a matter of layering controls on top of existing infrastructure. It requires a coordinated operating model that spans security architecture, engineering culture, vendor strategy, and regulatory posture. The six practices below represent the dominant blueprint of effective cloud security strategies adopted by leading institutions.

Prepare for emerging threats

Practical preparation starts with active threat intelligence. This means consuming sector-specific feeds, participating in information-sharing communities such as FS-ISAC, and translating intelligence into concrete detection logic. Threat hunting teams should operate continuously rather than only after incidents.

Red teaming and adversarial simulation belong to the standard control set. Purple team exercises, attack path mapping, and tabletop scenarios involving deepfake fraud, agentic AI intrusions, and destructive ransomware help validate that detection and response capabilities match the threats banks face.

Operate Zero Trust across hybrid and multi-cloud estates

Zero Trust is the only viable operating model for banks running workloads across on-premises systems, multiple public clouds, private cloud environments, and dozens of SaaS providers. The core principle is straightforward: never trust, always verify, and assume breach.

Identity is the foundation. Every access decision should evaluate the user, the device, the workload, and the context in real time. Phishing-resistant authentication, just-in-time privilege elevation, and continuous session evaluation replace the standing trust granted by traditional VPNs and network zones.

Micro segmentation should extend to cloud-native workloads. Lateral movement, the mechanism that turns a single compromised credential into a catastrophic breach, is contained when workloads can only communicate with explicitly authorized peers. Service mesh technologies and identity-aware proxies make this practical at scale, while strong cloud encryption across data in transit, at rest, and increasingly in use limits the value of any successful intrusion.

Mature DevSecOps with software supply chain integrity

Shift-left security measures put controls where developers work. Static and dynamic application security testing, infrastructure-as-code scanning, secrets detection, and dependency analysis all run inside CI/CD pipelines. Findings appear in the developer’s normal workflow, not in a separate ticketing system weeks later.

Software supply chain integrity has become a board-level concern. Banks must know what is in the software they run. This requires software bills of materials (SBOMs), signed and verified build artifacts, attestation of build provenance, and continuous monitoring of open-source dependencies for newly disclosed vulnerabilities.

Secrets management deserves particular attention. Hardcoded credentials in repositories, exposed API keys, and unrotated service account tokens are among the most common initial access vectors. Centralized secrets vaults, short-lived credentials, and automated rotation should be standard.

Manage concentration risk

Concentration risk operates on several dimensions. Provider concentration captures the impact of a single hyperscaler outage or compromise. Regional concentration captures the impact of a single availability zone or geographic event. Service concentration captures dependence on a specific managed service for which migration would be difficult.

Mitigation requires deliberate architectural choices. Multi-region deployments with active-active or hot-standby configurations protect against regional events. Workload portability, achieved through containerization and avoidance of provider-specific managed services where feasible, preserves the option to migrate. A well-designed hybrid cloud posture, combining public, private, and on-premises capacity, gives banks the flexibility to balance performance, cost, and resilience.

Evolve cloud governance to risk-based assurance

Risk-based assurance reframes the question. Rather than asking whether every control is documented and reviewed on schedule, it asks where the highest residual risks are and whether the security controls working against those risks are effective.

Continuous control monitoring replaces point-in-time audits. Automated evidence collection, integrated with cloud-native logging and posture management tools, provides assurance that controls are operating as designed every day rather than once a year. Exceptions are surfaced when they occur, not when an auditor finds them months later.

Embed regulatory engagement

Banking is one of the most heavily regulated industries in the world, and regulatory compliance in the cloud has moved squarely into the supervisory spotlight. Frameworks such as DORA in the European Union, the FFIEC guidance in the United States, the PRA expectations in the United Kingdom, and the MAS guidelines in Singapore all impose detailed compliance requirements on cloud risk management, third-party oversight, and operational resilience.

Engagement with regulators should be proactive rather than reactive. Banks that treat supervisors as informed partners, sharing their cloud strategies and inviting feedback early, tend to encounter fewer surprises during examinations. Regulators increasingly value transparency over polished narratives.

Regulatory technology can ease the load. Mapping internal controls to multiple overlapping frameworks, automating evidence generation, and maintaining audit trails across cloud environments are all increasingly handled by dedicated tooling rather than spreadsheets.

FAQ

Rethinking cloud security in the banking market

The banking industry is not going to leave the cloud. The economic and competitive pressures that drove the migration are still there, and intensifying. The regulatory regimes that once urged caution have, in most major jurisdictions, accepted cloud computing as essential financial infrastructure and now concern themselves with operational resilience rather than location.

The institutions that absorb that point soonest, and rewire their security operations to match, will spend more in the short term. They are likely to spend less resources in the long run. The forecasts agree that the market will keep growing. The harder question, for the banks doing the spending, is whether the controls they are buying are the ones a Mythos-class adversary will encounter, or the ones designed for a slower, less inventive world that no longer exists.

The threats reshaping banking cloud security are evolving faster than ever. If you would like an independent assessment of your readiness for AI-driven attacks, please schedule a consultation.

AI fraud detection in banking: use cases and solutions

Your business results matter

Achieve them with minimized risk through our bespoke innovation capabilities. Fill in the form below.