Software engineering

services for BFS

Avenga’s financial software engineering solutions

Every financial organization has its own vision for the future. At Avenga, we co-create digital solutions to reflect your business goals, your clients’ expectations, and BFS realities.

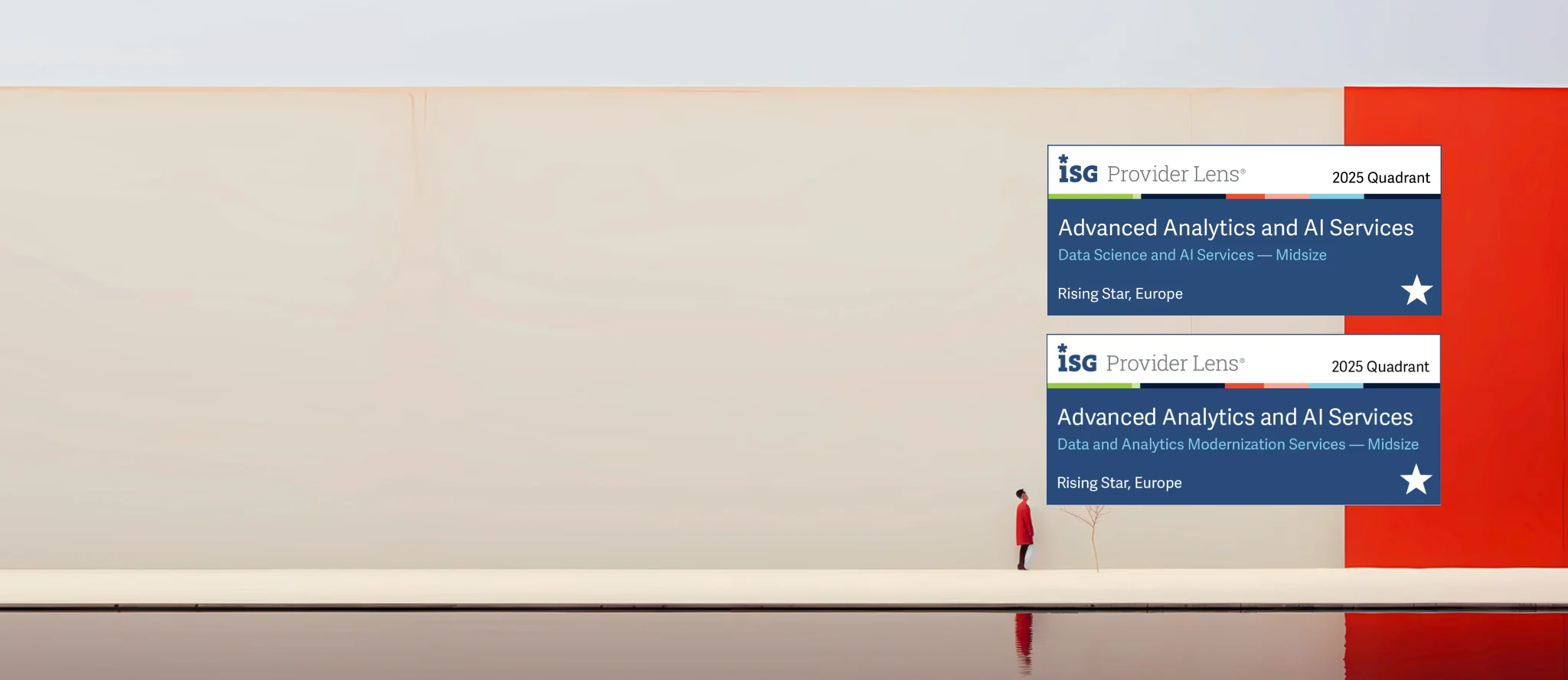

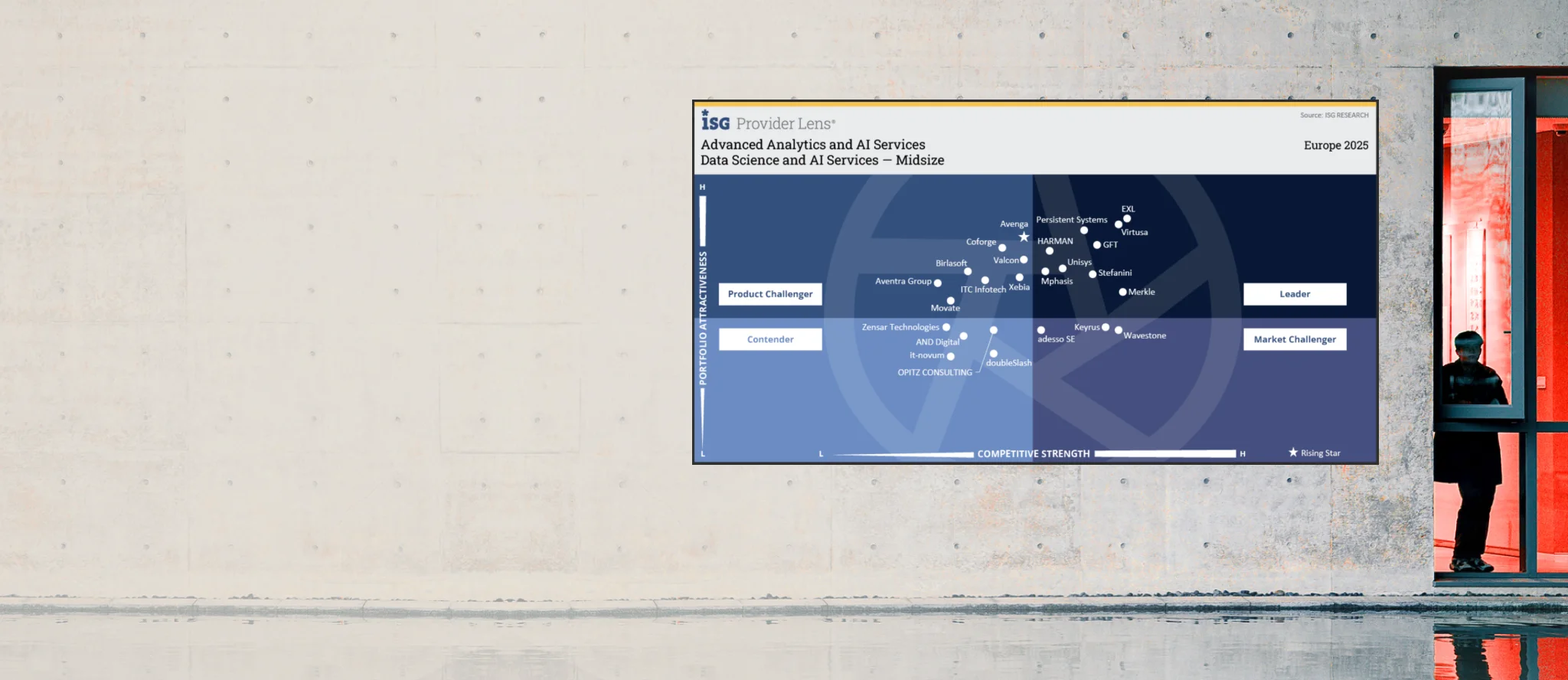

Uncover the real BFS data value. Avenga builds AI-driven data integration engines, predictive analytics, fraud detection, conversational banking.

Great banking feels personal thanks to great CX. We blend AI, unify data, create customer journeys, and omnichannel engagement processes.

Flexible platforms grow with you. We modernize legacy systems and apps, integrate tools, and streamline cloud adoption to boost your company.

Leverage cybersecurity and compliance solutions. We protect your data, strengthen compliance, and keep your institution resilient against evolving cyber threats.

Trusted by financial institutions around the globe

Financial software solutions with the Avenga difference

Our clients see Avenga as an extension of their own teams — curious, engaged, and driven by shared outcomes. We dive deep into your operations, adapt to your pace, and bring fresh thinking to every challenge.

-

Bold moves, real impact

Financial institutions leap ahead with our cloud services, API, automation, AI, UX/CX, innovation labs and more — we deliver everything that brings measurable results because only bold solutions ensure real impact.

-

Change that performs

Breaking free from legacy constraints gives our clients freedom to create exceptional finance experiences. Whether it’s untangling legacy spaghetti or accelerating to cloud-native agility, we introduce change that performs.

-

Determination and focus

Our 24/7 SOC coverage, automated compliance, and zero-SLA-breach performance ensure true resilience. We maintain and strengthen systems, keeping your financial operations secure, stable, and always ready for what’s next.

Software solutions supporting businesses

-

-

-

Case Study · February 20, 2026

Case Study · February 20, 2026Slashing review cycles by 86% with automated fraud detection

-

Case Study · November 20, 2025

Case Study · November 20, 2025Delivering 100% system compatibility for Ayasdi’s ML infrastructure

-

Case Study · November 10, 2025

Case Study · November 10, 2025Integrated cloud solution streamlining operational agility

-

Case Study · June 18, 2025

Case Study · June 18, 2025EasyFinancing Invoice Handling Automation Tool

-

Case Study · June 18, 2025

Case Study · June 18, 2025Trōv: Advanced BI Solution

-

Case Study · May 15, 2025

Case Study · May 15, 2025Complex Insurance Products Digitalization

-

End-to-end financial engineering capabilities

-

AdTech and MarTech

Power smarter customer acquisition and loyalty with compliant, data-driven AdTech and MarTech ecosystems built for finance. We help BFS brands personalize engagement, automate campaigns, and deliver measurable ROI across every touchpoint — all with enterprise-grade security and precision.

Learn more

-

Avenga Experience

Turn complex financial processes into intuitive, human-centered journeys. With strategic analysis, visualized requirements, and UX-driven design, we align your teams, simplify decisions, and create digital experiences that strengthen trust and accelerate customer satisfaction across banking and financial services.

Learn more

-

Data and AI

Make every decision intelligent. We engineer AI-powered analytics, customer experience, fraud detection, ESG insights, and strong governance frameworks that give financial institutions clarity, speed, and confidence — from risk forecasting through improved customer experience to compliant data management.

Learn more

-

Intelligent automation

Automate the heavy lifting in banking and financial services. We streamline KYC/AML, claims, underwriting, loan processing, and customer operations with secure, scalable automation that reduces costs, eliminates errors, and keeps compliance effortless.

Learn more

-

Managed services

Ensure uninterrupted banking operations with engineering services built for resilience. Our 24/7 monitoring, proactive optimization, and zero-SLA-breach culture keep your platforms secure, stable, and performing at the speed your customers expect.

Learn more

-

Product engineering

We design, develop, and evolve secure digital banking platforms, mobile apps, trading tools, payment solutions, and more — combining cloud, AI, and modern architectures to deliver future-proof innovation for BFS leaders.

Learn more

Related content

AI for credit risk management: Embrace banking innovation in 2026

AI and its role in the banking industry

FAQ

Speak to our expert

Let’s ensure your financial institution leaps ahead.

Lenka Votavova

Head of Marketing BSFI & LeadGen Global Marketing