Open banking APIs explained: How bank APIs work

June 3, 2026 8 min read 124 views

APIs have quietly rewritten the rules of banking. They let organizations in the financial industry exchange data securely and instantly. The result is open banking, a model where customers control their financial information and choose how it’s used. This article explores how open banking API technology works, the benefits it brings to customers and institutions, and the strategic models banks use internally and externally.

Open banking and API landscape

The financial landscape is being reshaped with open banking. And it is revolutionized by APIs. Such a transformative movement redefines economic data sharing and service delivery. It paves the way for interconnected and innovative banking ecosystems to emerge, moving well beyond the limitations of traditional banking.

The advent of open banking

Open banking marks a new era in finance. Now, banks share data through APIs. This paradigm promotes transparency as well as introduces a new way toward consumer empowerment and customized financial services.

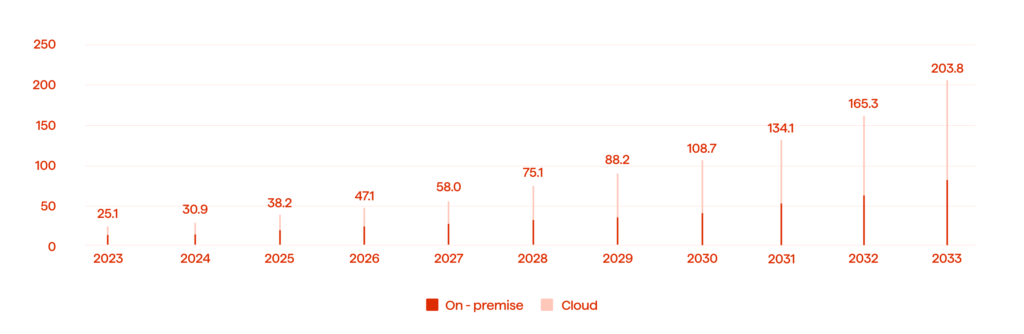

More and more banks and financial institutions understand that and adopt an open banking philosophy and solutions (see Figure 1).

Open banking gives consumers more control and freedom over their financial data. Financial institutions can offer customized products and services using open APIs. APIs help meet customers’ diverse financial needs. For example, with open banking APIs, a customer’s bank can permit third parties to aggregate that individual’s financial data across multiple institutions, offering a consolidated view of finances or suggesting better financial products.

Regulations such as the Payment Services Regulation (PSR) and PSD3 in the European Union influence the drive towards open banking. Building on the foundation laid by PSD2, the new framework compels banks to allow secure access to customer financial data for authorized third-party providers with explicit customer consent, while introducing stricter rules on fraud prevention, API performance, and fair access to payment systems. Strong customer authentication remains a cornerstone of these requirements, ensuring that every data exchange and payment initiation is properly verified.

The regulatory push complements the financial industry’s evolving data-sharing standards and the move toward open finance, which extends data access beyond payments to savings, investments, and insurance. Together, these measures ensure effective, transparent, and safe interaction for all parties involved.

A pivotal role of APIs

At the core of open banking lies the application programming interface. It is a foundational technology enabling this financial revolution. APIs enable secure data exchange between banks and third-party providers. To illustrate, APIs serve as secure messengers, allowing banks to transmit customer financial data, including account balance information and transaction histories, to authorized third-party apps for services like budgeting and investing. It’s like giving a key to a trusted friend to access your shared space safely.

APIs are crucial for open banking. They enable easy connections between banks, fintech, and other services. APIs define software interaction protocols, enabling the sharing of banking data. This data helps create innovative financial services. For instance, a bank’s API could allow fintech companies to initiate payments on behalf of customers directly from their bank account, streamlining the payment process and offering enhanced customer convenience.

Benefits of banking APIs

Banking APIs offer many benefits, such as establishing new customer engagement and financial innovation standards. The APIs simplify operations. That is vital for two key aspects: better customer experience and going toe-to-toe with the ever-changing economic landscape.

Hyper-personalized customer experiences

Customers no longer compare their bank to other banks. They compare it to every digital product they use daily. APIs make it possible to deliver tailored insights, real-time financial dashboards, instant payments, and AI-powered recommendations across mobile apps, wearables, and even voice assistants, creating a seamless user experience at every touchpoint. Industry research consistently shows that the majority of banking customers expect personalized, proactive financial guidance, and institutions that deliver it see measurably higher engagement, retention, and cross-sell rates.

Faster innovation and time to market

APIs let banks build, test, and launch new services in weeks rather than years. Embedded finance, buy-now-pay-later integrations, real-time payment rails like SEPA Instant and FedNow, and AI-driven credit decisioning have all scaled rapidly thanks to API-first architectures. Banks like BBVA, DBS, and Goldman Sachs have built entire banking platforms around exposing their capabilities through APIs, turning previously siloed services into modular products that partners can integrate on demand.

New revenue models and ecosystem partnerships

Open APIs have turned banks into platforms. By exposing services to fintechs, retailers, and SaaS providers, banks earn revenue through API monetization, partnership fees, and Banking-as-a-Service (BaaS) offerings. This shift has opened the door to embedded finance where modern banking solutions live inside non-bank products like e-commerce checkouts, accounting software, and payroll platforms.

Strategic API models in banking services

In fintech, APIs catalyze efficiency and market expansion, beyond technological tools. Their deployment within financial institutions signifies a commitment to innovation and future-proof operations. The most common use cases range from internal automation to large-scale ecosystem partnerships.

Internal APIs for operational efficiency

Internal APIs in banking connect old systems to new apps for tasks like fraud detection and identity verification. This integration aids real-time service. The APIs reduce operational overhead and boost financial services agility. For instance, banks that use APIs for credit assessments can streamline application processes, leading to measurable cost savings and a quicker turnaround for customers.

External APIs for ecosystem expansion

Open APIs help payment systems evolve. Banks collaborate with fintech companies to offer direct account-to-account transfers, drawing on transaction data shared securely between systems. An exemplary use of external APIs is seen in the collaboration between incumbent banks and payment initiation service providers (PISPs), which enables secure and direct online payments, bypassing traditional card networks and reducing transaction fees. In this way, APIs allow financial institutions to extend their reach far beyond their own apps and channels.

External APIs facilitate innovation and collaboration, supporting growth in the digital economy. They meet evolving service needs.

Challenges and considerations

Integrating open banking APIs brings innovation but also comes with challenges. Figuring around the workarounds within these obstacles is pivotal in ensuring the sustainability and security of the API-driven banking transformation.

Here are the challenges one should mention:

Legacy system integration

Many financial institutions struggle to integrate modern APIs into their aging banking infrastructures. These older systems are often resistant to change, which makes the process of updating them to be API-compatible both complex and resource-intensive.

However, banks are taking proactive steps to modernize their systems by investing in technology upgrades and partnering with fintech companies to bridge the gap between old and new. Some central banks have successfully launched digital-only branches built on modern tech stacks that seamlessly integrate with APIs, indicating a promising direction for the future of digital banking.

Data security and privacy compliance

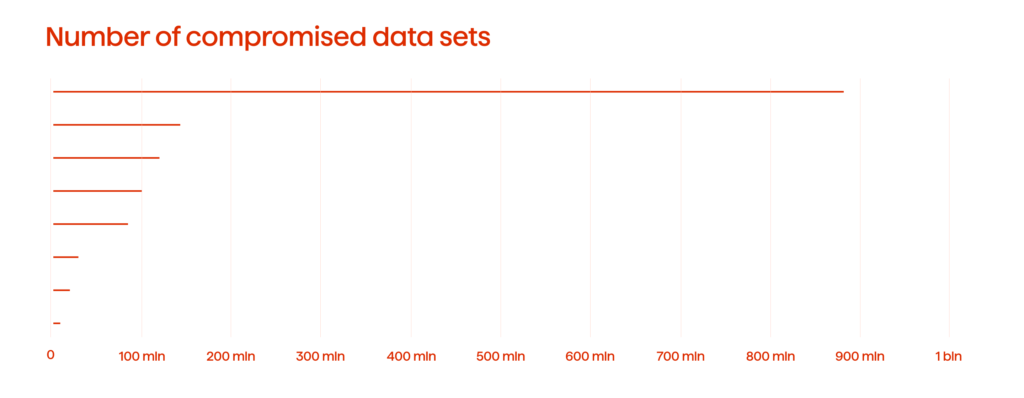

As open banking APIs become more common, protecting customer data and complying with privacy regulations is more important than ever. Banks need to balance encouraging innovation while carefully safeguarding sensitive information, including every detail tied to a user’s bank account. This presents the utmost importance considering the scale of data breaches in the financial sector (see Figure 2).

The financial industry must take extra precautions to meet GDPR and DORA. They must encrypt API traffic, regularly audit access controls, and establish clear data usage policies. This has led to the creation of advanced security solutions like tokenization and dedicated API gateways to secure customer data handling.

To stay successful in this new era of open banking, banks must create an environment that fosters innovation without compromising security or privacy. This is essential to maintain customer trust in the long run.

FAQ

The future shaped by open banking APIs

The journey through open banking shows APIs are keystones of a banking renaissance. From enhancing customer experiences to pioneering new services, APIs have demonstrated their transformative power. The banking sector is evolving due to dynamic interfaces. Growth and innovation potential seem limitless. The future of banking, underpinned by APIs, holds the promise of a more inclusive, responsive, and interconnected financial ecosystem.

Start a conversation with our team and discover how a partnership can future-proof your banking infrastructure.

Your business results matter

Achieve them with minimized risk through our bespoke innovation capabilities. Fill in the form below.