AI in insurance claims management: A practical guide to enhanced claim processing

July 20, 2026 12 min read 168 views

AI can dramatically expedite claims processing, given that the insurance carrier already has the foundation for its implementation.

Artificial Intelligence (AI) presents insurance carriers with a distinct competitive advantage. For organizations with the appropriate foundation in place, it accelerates claims processing and improves accuracy across the function. The timing is favorable. Data continues to grow in scale and complexity, and carriers that deploy AI convert that growth into more effective risk management. Several have already demonstrated the value. Their automation extends beyond isolated tasks to support the entire claims workflow. Insurers that follow can equip their knowledge workers with stronger capabilities, meet rising client expectations, and lead in an evolving market. The result is a clear path toward greater efficiency and stronger customer relationships.

Why insurers are turning to AI for data management

Some carriers still collect data on paper or in non-standardized, unstructured digital formats, even inside operations they consider modern. This leaves employees, and claims adjusters in particular, without immediate access to the information they need when a decision has to be made. Productivity suffers, and costly errors follow. Reviewing and extracting insights from data spread across many platforms, formats, and structures by hand is slow and prone to mistakes. Procedures built this way cannot keep pace with business growth. That gap explains why a growing number of executives across the insurance industry now look to AI to manage their data assets.

From our experience, AI is an invaluable tool for giving insurers a consolidated view of their clients. It can unify the historically disparate datasets that define the insurance domain and open access to critical insights for personnel working across the claims lifecycle.

That transparency changes what a carrier can offer. New customer journeys take shape around the client, informed by a clearer picture of their preferences and life circumstances. This agility strengthens customer relationships through better experiences, and it supports personalized quotations, policy recommendations, and targeted offers at every touchpoint. Together, these gains point to measurable improvements in the bottom line, and higher customer satisfaction follows.

Key use cases of AI in claims insurance

AI can automate much of the administrative work that surrounds claims management. AI models handle both numerical data and natural language. AI-enabled tools search through knowledge bases, healthcare forms, policies, and related documents to retrieve the information an adjuster needs. These models strengthen the work of claim handlers. They help staff identify eligible claims, flag signs of possible fraud, and apply consistent judgment on how much of a claim should be paid.

Common use cases include:

- Document intake and extraction. AI reads submitted forms, policies, and correspondence, then pulls the relevant details into a structured format. This is often the first stage of claims intake.

- Claims triage. Models sort incoming claims by complexity and route each one to the appropriate team or workflow.

- Eligibility verification. Algorithms check claims against policy terms to confirm coverage before adjudication begins.

- Fraud detection. Machine learning models scan claims for patterns that indicate potential fraud and flag them for review.

- Damage assessment. Computer vision evaluates photos of damage and supports faster loss estimates.

- Claim status responses. A chatbot or virtual AI agent answers routine status inquiries without adjuster involvement.

- Payout calculations. Models apply policy rules and prior data to determine settlement amounts with greater consistency.

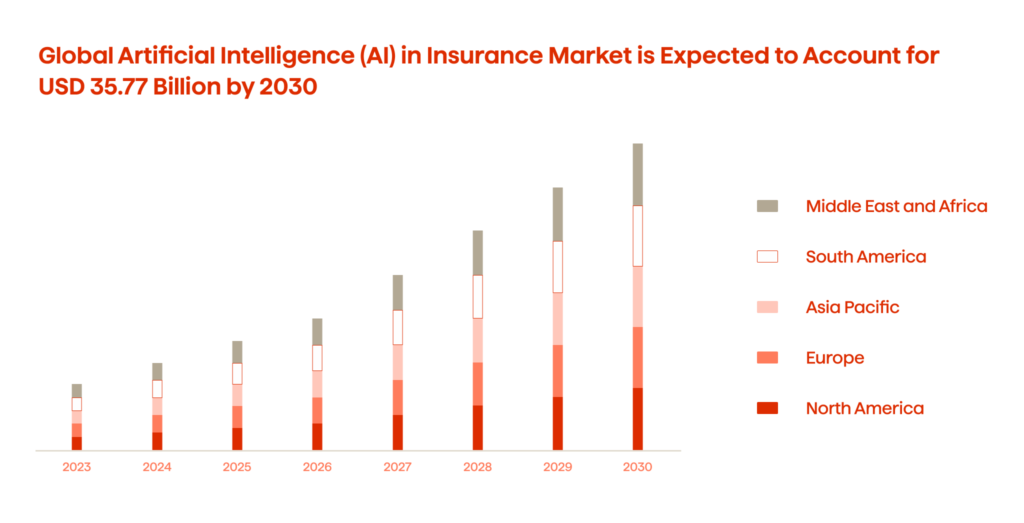

The global use of AI in the insurance market is expected to reach USD 33.77 billion by 2030 (Figure 1).

Currently, approximately 30% of a knowledge worker’s time is dedicated to locating and retrieving data from various sources. These technologies enhance staff effectiveness. By handling tasks such as data entry, claim routing, and document review, they free valuable time for higher-value work. This is one of the clearest benefits of claims automation.

What’s changing in insurance claims processing?

At present, approximately 31% of claimants express that they are not satisfied with the handling of their claims. This figure constitutes a substantial portion of a carriers’ client base, and the potential loss of these customers’ renewal premiums could translate into an estimated $170 billion in financial setbacks over the ensuing five years.

According to a Global Insurance Market Report (GIMAR), the main cause of this dissatisfaction is, somewhat unexpectedly, not primarily the amount disbursed in a settlement, although that plays a role. Rather, the issue revolves around the speed of the claims process and the intricacies involved in navigating its various stages. Better claims handling addresses both.

An equally pertinent statistic underscores that approximately 40% of inbound calls are straightforward requests for claim status updates. These routine inquiries represent a category where AI can competently and autonomously respond, optimizing operational efficiency for many insurance companies.

The challenges claim adjusters face

Indemnity accuracy

Accurate indemnity valuation has consistently been one of the most formidable challenges for claims adjusters, for several reasons. Achieving precision in loss valuation demands navigating a landscape shaped by vague policy language, frequent gaps in underwriting and claims assessment, the need for vigilant fraud management, and an ever-changing regulatory environment. With so many dynamic variables at play, the process becomes daunting as adjusters try to balance accuracy against operational efficiency. Escalating inflation, chip shortages, and supply chain disruptions compound the difficulty. The power of AI is well suited to this kind of complexity.

Manual processes

The second key challenge is the manual processes many carriers still rely upon. The handling of paperwork, unstructured digital documents, and communication with all involved parties often consumes enormous amounts of an adjuster’s time. Also, manual data entry and calculations are prone to errors and inaccuracies. Subsequently, these issues can lead to disputes with claimants, cause undue delays, and result in additional administrative work. Besides that, outdated procedures are often the cause of inconsistencies, unequal workloads, inefficient resource allocation, and increased overheads.

Fragmentation of experience

An often-cited analogy is that while many insurers have built digital highways, there are still frequent manual off-ramps every ten feet. Although some digital processes have been integrated into the workflow, such as claimants uploading images of their damaged vehicles to the carrier’s app, these processes still typically require adjuster intervention, often by phone, as the next step. As a result, the overall experience remains fragmented, which introduces further challenges in the context of disabilities, group benefits, and other complex claims.

Customer expectations

Expectations around claims management continue to rise. Shifts in customer behavior, combined with competitive pressures, have created an environment where claimants anticipate swift service and a streamlined process. To thrive, carriers must implement higher levels of automation, adopt AI and related technologies at greater scale, and place stronger emphasis on customer-centricity. AI is transforming how carriers meet these expectations.

Is there a faster path to resolution in claim management with AI?

Within large insurance organizations, unnecessary delays persist across many phases of claims processing, particularly for straightforward claims. These delays often stem from long turnaround times as claims move between teams. The disjointed stages increase customer inquiries and add steps to the process. Even for high-end claims, where extended adjudication and filing stages are expected, substantial optimization opportunities remain. Delivering a faster claim outcome is achievable where AI is properly implemented.

How we approach the AI-enabled claims processing transformation

Our approach to the AI-enabled claims processing transformation at Avenga begins with the optimization of the First Notice of Loss (FNOL) and the entire claims lodgement phase. AI technology, sometimes complemented by Robotic Process Automation (RPA) bots, is perfect for expediting eligibility checks based on policy matching, providing policy explanations and guidance, and ensuring prompt handling of basic checks during the initial claim submission. As claims information is not typically structured in a manner that allows claims teams to easily retrieve answers to specific questions that are needed to advance the resolution, AI algorithms are employed to retrieve, summarize, and categorize the complex documentation required.

The next logical steps, therefore, are:

- Simplifying and accelerating initial data intake through various channels such as web portals and mobile applications (for which chatbots and other Natural Language Processing (NLP) technologies are used).

- Establishing a robust backend infrastructure to support AI algorithms that are capable of verifying covered events, predicting claim complexity levels, identifying potential high-cost claims, and calculating the likelihood of litigation.

When it comes to adjudication, the process is frequently characterized by labor-intensive demands. Even in the case of straightforward claims, personnel are required to meticulously review claims and their associated documentation, calculate the extent of loss, engage with claimants across various communication channels, potentially delve into prior interactions if they are on record, and undertake a substantial volume of data entry tasks.

We use AI to streamline this complex procedure, turning to a simple binary determination for the algorithm. Specifically, we employ Generative AI (Gen AI) for collecting preliminary info, extracting relevant data from various sources, and categorizing pertinent documents. Computer Vision (CV) models then evaluate damages based on the visual evidence a claimant provides, and specially trained fraud-detection ML algorithms identify potential fraudulent activity. Used separately or together, in any configuration that suits the carrier’s requirements, an AI system of this kind can significantly improve operational efficiency and accuracy.

Insurance carriers must maintain a comprehensive understanding of the AI model’s inherent limitations. Regardless of the technological advancements achieved, there will still be certain categories of claims, notably those of a highly emotional, large-scale, or complex nature, that will forever remain out of the scope of what AI can handle. Examples of these include ENO (Errors and Omissions), DNO (Directors and Officers liability) in the commercial domain, and severe accidents in the realm of life insurance.

In this area, the strategic focus lies in optimizing specific parts of the process. That means automating select stages while reserving human intervention for cases that require manual exception handling. High-frequency, low-complexity claims are strong candidates for straight-through processing, while sensitive cases stay with a person.

As we transition to the culminating phases of claim resolution ᅳ settlement and closure ᅳ AI presents an array of promising prospects. Settlement manifests in several diverse forms, ranging from financial disbursements to repairs or replacements. Each of these scenarios triggers distinct workflows, necessitating discrete steps. For instance, in the case of a financial payout, claim management systems of record must be consulted, and payment mechanisms must be promptly activated to compute the requisite amounts and facilitate fund transfers to either claimants or repair entities.

When the context pertains to component replacement or repair, our supply chain management solutions ensure the delivery of essential materials. Through integration with our existing platforms, AI has enabled us to automate the majority, if not the entirety, of these processes, particularly within high-frequency and low-complexity claims. Human intervention is reserved for scenarios that warrant exceptional scrutiny. This is a practical model for insurance claims automation.

If the downstream tasks are API-compatible, we deploy ML-driven orchestration tools. When integration with less flexible legacy systems is required, we apply AI-driven process automation. The right AI solution depends on the systems already in place.

An equally vital aspect of the settlement phase pertains to client engagement and communication. Leveraging GenAI-enabled communication tools, we expeditiously disseminate notifications across the channels preferred by our clients. This approach substantially alleviates the burden on our clients’ contact centers, enhances customer experience, and maintains their clients being well-informed about the progress of their claims.

AI can also support automated claims review at the final closure step. We have had considerable success helping carriers use predictive models to identify areas for process improvement and important trends in claim categories and associated costs. The same models surface comprehensive insights and recommendations on optimal offers and policy enhancements. This is where the value of AI claims review becomes most visible.

FAQ

Implementing AI to achieve claims automation

AI continues to move deeper into insurance despite the industry’s stringent regulatory frameworks. Algorithms are already in use by many carriers worldwide, including our own clients, to help adjusters make faster and more accurate decisions. Growing adoption of technology in the insurance industry reflects this shift.

As adoption grows, the implications become more significant. Predictive AI models hold immense promise in helping carriers fight fraudulent claims. The more insurers use these tools, the greater the collective effect.

They can also reduce processing time for simple routine claims from days to seconds, provided the organization has the infrastructure and integrations in place to support end-to-end automated workflows. Implemented correctly, effective claims automation frees adjusters to focus on higher-value work and drastically elevates efficiency.

Turn your claims operation into a source of measurable savings and stronger retention. Avenga can help you build the foundation. Contact our specialists to explore what is possible.

Your business results matter

Achieve them with minimized risk through our bespoke innovation capabilities. Fill in the form below.