AI for credit risk management: Embrace banking innovation in 2026

February 26, 2026 11 min read 342 views

Integrating AI and ML within the banking sector, especially in credit risk management, represents a pivotal shift towards more sophisticated and efficient financial services. These technologies have become topics of extensive discussion among professionals and are central in reshaping how banks assess and manage credit risk.

The combination of AI and ML provides unparalleled insights and automation capabilities, enhancing the accuracy of credit decisions and risk assessments. As quoted by a leading industry expert, “As technology evolves, it’s evident that AI and ML are not just fleeting trends but are integral to the future of banking.”

Through trial and error, AI and ML in credit risk management are paving the way for broader applications across various financial sectors, including wholesale banking, retail banking, insurance, wealth management, and capital markets. The next step is thoroughly exploring AI and ML applications in credit risk management.

AI in credit risk key takeaways

- AI can automate many lending decisions across acquisition, credit decisioning, monitoring, servicing, and collections, freeing teams for higher-value work.

- Model performance relies on reliable financial data, robust validation, and ongoing monitoring to prevent drift and hidden bias.

- Explainability isn’t optional: banks need transparent outputs (reason codes) to support customer trust and regulatory expectations.

- The future of credit is model-led, but trust-led: winners will pair AI speed with governance, fairness, and human oversight.

How artificial intelligence is reshaping the credit lifecycle

A surge in adoption reflects the significant value that AI and ML add across the entire credit spectrum. From preliminary risk assessment to ongoing account management, these technologies facilitate a deeper understanding of borrower behavior, improve prediction accuracy, and streamline operational processes. Recent studies underscore this trend, with AI in the banking market projected to experience exponential growth.

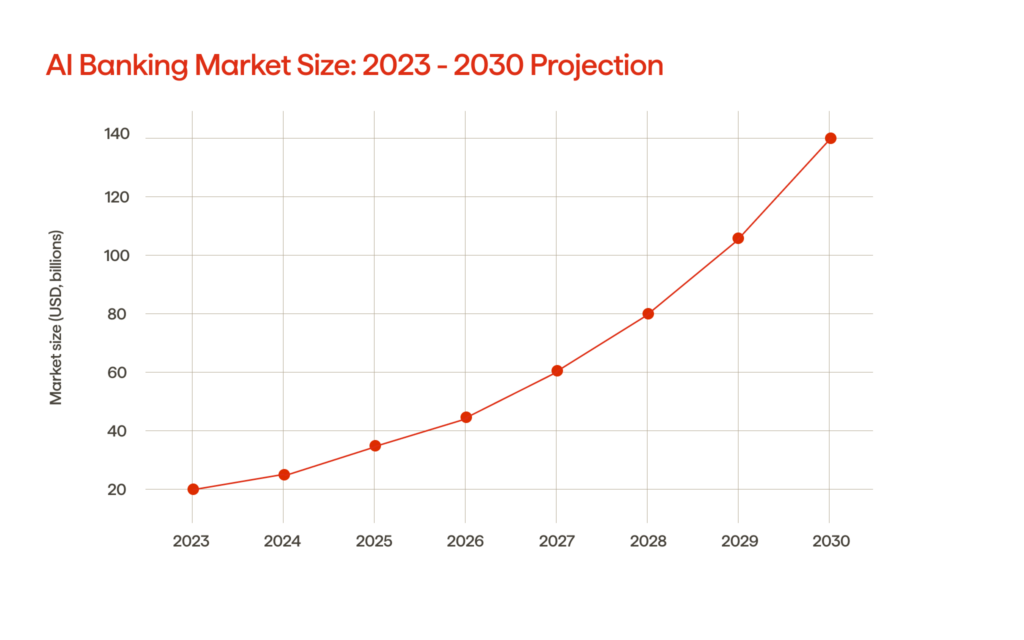

Evidence of this new progressive approach to banking and credit is seen in the estimated value of the global AI banking industry, which was approximately USD 19.87B in 2023 and is projected to reach a value of approximately USD 143.56B by 2030, based on an average annual compound growth rate (CAGR) of approximately 31.8%.

Regardless of any prediction, one thing is clear – AI and ML in banking will continue to be further applied and generate massive revenues.

Financial institutions utilize machine learning capabilities to score credit applications based on more comprehensive data signals (e.g., cash flow patterns and transaction context), thereby automating the minutiae of manual credit checks that typically take several business days to complete. Results from model outputs are used for continuous monitoring of applications through early warning alerts, dynamic limit adjustments, and collection strategies prioritizing optimal outreach during optimal times.

One of the keys to making AI successful in regulated lending is to employ more explainable methods of AI (e.g., reason codes, feature attribution), apply governance standards for robust model development, and conduct ongoing validation testing to monitor for bias and drift over time. When done correctly, AI accelerates informed decisions and empowers teams to trace, defend, and refine their decision-making process.

Achieve unparalleled growth with Avenga’s tailored digital banking solutions.

Building AI-driven credit risk models on reliable financial data

Conventional credit risk analysis often relies on complex statistical models that assume formal relationships between features in mathematical equations. AI uses ML methods that can learn from data without requiring rule-based programming. As a result of this flexibility, ML methods can better fit the patterns in data. It is done through the following classical ML algorithms and deep learning techniques:

- Logistic regression: one of the most commonly used ML algorithms. It’s a supervised learning approach, which means that a user feeds pairs of input indicators and desired outputs into the algorithm during training, and the algorithm learns to produce the desired output given a specific input. Afterwards, the trained model can predict the output given new and unseen input without any help from a human. At the heart of the Logistic Regression model is a linearity assumption; thus, it can only model simple linear dependencies.

- Random Forest Method: an intuitive supervised learning method. Here, the idea is to leverage historical datasets and build them into data trees to optimize the future analysis process.

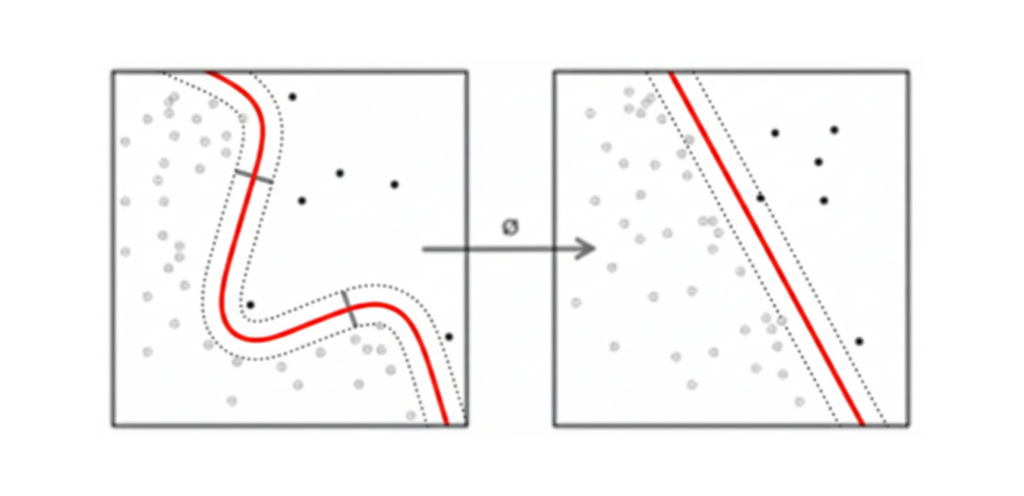

- Support Vector Machine (SVM): a vanilla SVM is a type of linear separator. We draw a straight line through our data to separate it into two classes, dividing it in half. If we can’t draw a line through the data, we can transform the data so that the separation becomes possible.

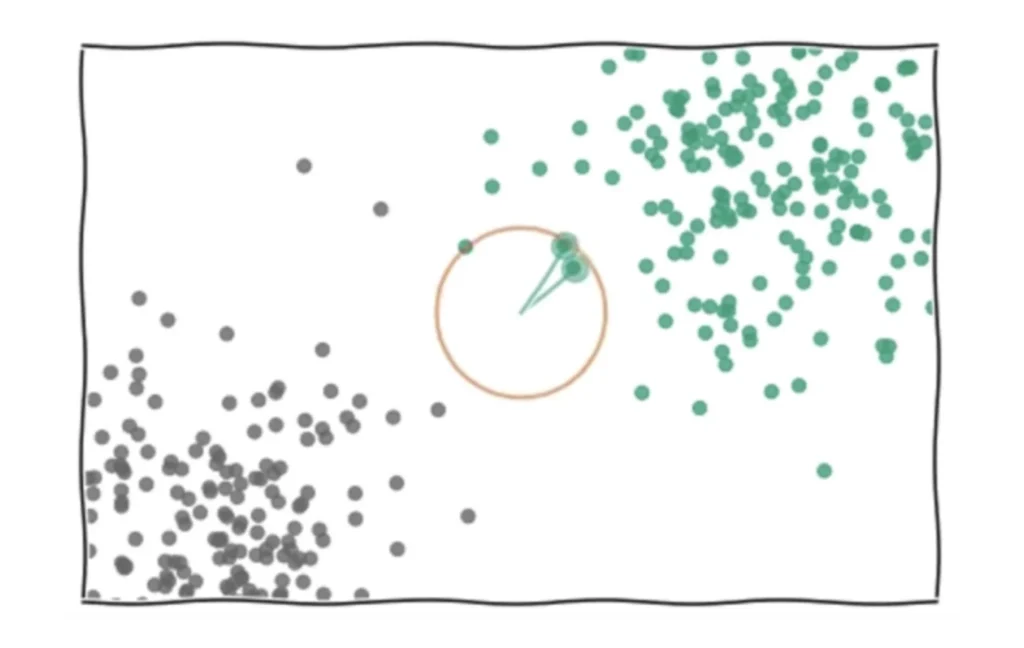

- K-Nearest Neighbors (KNN): finding the class of the data based on proximity to old data. Tell me who your closest friends are, and I will tell you who you are.

- Neural networks (NNs) – basically, these are algorithms mimicking the way the human brain operates. NNs are effective, especially for short-term predictions. They are also robust in the sense that they effectively handle missing data and correlations between input variables. However, NNs are not easily interpretable, thus it is difficult to understand why the model makes the predictions it does.

These tools enable the equitable distribution of data and foster an environment for analyzing non-linear patterns of different variables, such as those used in credit scoring. As a result, banks receive more accurate credit risk analysis than traditional statistical methods.

Where AI solutions help most in practice

AI and ML enable institutions and organizations to work with real-time transactional data. It also provides models that can operate with a wide range of data points. By considering all these factors together, AI and ML offer several notable use cases.

Automated and personalized decisions across a customer’s lifecycle

Financial institutions can use AI models across various use cases. This approach adds value by automating several decisions linked to diverse customer journeys. For instance, within the initial stage of the lifecycle, banks can utilize AI analytics to enhance aspects such as customer acquisition, relationship deepening, and intelligent servicing. AI makes a customer’s journey seamless and more appealing for these factors alone.

Better credit lending

When financial institutions focus their efforts on implementing AI in areas where they expect to see the most significant benefits, they can automate over twenty different types of decisions across multiple stages of the customer journey. In particular, during the lending lifecycle, AI can help automate over 20 decisions across various customer journeys. It demonstrates its most significant benefits in customer acquisition, credit decision-making, monitoring and collections, building stronger customer relationships, and providing enhanced service. With the advances being made in AI and ML to support credit risk management, banks will be able to improve their risk assessment processes by combining multiple data sources to create a more comprehensive risk profile.

Negligence and fraud detection

With credit relationships rapidly shifting to digital channels, AI enables the automated processing of various aspects of loan applications, credit approvals, and fund reimbursements. However, the more loans a bank can issue, the higher the possibility of fraud. At this point, many institutions are integrating AI-based tools that help recognize negligence in its initial stages.

For example, McKinsey cites the case of Ping An. This company utilizes an image analytics model to identify several dozen facial microexpressions in its clients, determining whether they are being truthful in their loan applications. This shows that AI can process various data points to increase the number of clients while decreasing fraud.

Optimization of the collections process

Sending a debt to collections is among the last things a lender wants to do. This is because third-party fees from various collection agencies quickly absorb any margin. Furthermore, clients who receive a collections class are less likely to return to the lender. The reports show that acquiring a new client is five times more expensive than keeping an existing one. This also means that optimizing the collection process can increase customer retention and save companies a significant amount of money.

With AI technologies, institutions collect data points throughout the customer lifecycle. It presents a clear picture of who is most likely to repay a loan. If an institution receives a red flag, indicating that a customer is falling behind on their payments, specific actions can be taken to get them back on track.

Dynamic risk modelling

Unlike traditional models, ML algorithms can dynamically adjust to new information, learning from each interaction and transaction. This adaptability enables banks to continually refine their risk models, ensuring they remain accurate and relevant as market conditions change. Dynamic risk mitigation leads to more resilient financial systems that can withstand economic fluctuations and evolving risk landscapes.

Customized financial products

ML algorithms deeply analyze customer data to understand individual preferences, behaviors, and risk profiles. This analysis enables banks to design customized financial products that cater to specific customer needs, thereby enhancing satisfaction and loyalty. Customization can range from personalized loan terms to tailored insurance products, improving customer experience.

Operational efficiency and cost reduction

By automating routine tasks and decision-making processes, ML significantly reduces operational costs and enhances efficiency. Automated credit scoring, risk monitoring, and document processing speed up these processes and reduce the likelihood of human error. The efficiency gains from ML can be redirected towards strategic areas, such as customer service and product development, further enhancing a bank’s competitive edge.

Risks, controls, and regulations on the road to the future of credit

When AI tools are introduced into real-world environments, such as credit risk management, it’s essential to remember that the most significant risks they face are not necessarily “AI versus humans” but rather issues related to bias, opacity, and weak governance. These systems inherit bias from overly skewed (or unrepresentative) training data, can drift over time based on borrower activity changes, and can be rendered unexplainable if the regulator(s) or customer(s) ask why something happened or was assessed.

That’s why leading banks wrap AI systems in controls borrowed from classic model governance: independent validation, stress testing, monitoring for drift, clear ownership, and audit trails. U.S. regulators emphasize model risk management practices (e.g., OCC guidance tied to SR 11-7 principles), which prompt banks to document assumptions, validate outcomes, and manage third-party models in the same manner as other high-impact systems.

On the compliance side, the CFPB has made it explicit that lenders must still provide specific reasons in adverse action notices, even when decisions are made using complex algorithms. In the EU, the AI Act categorizes creditworthiness assessment as a “high-risk” use case, thereby raising the standards for governance, data controls, transparency, and human oversight. Frameworks like BCBS 239 emphasize the importance of robust risk-data aggregation and reporting when AI relies on extensive financial data pipelines.

FAQ

Final words: the future of credit is model-led, but trust-led

AI in banking has evolved from theoretical concepts to practical tools with widespread applications, including credit risk management and beyond. Today, the potential and application of AI and ML are universally recognized, enabling global-scale innovations. The adoption of these technologies extends far beyond banking and credit risk management, promising endless possibilities for those who leverage them.

Embracing AI now offers businesses a crucial early mover advantage, ensuring competitiveness in FinTech and other sectors. The question is not if companies can afford to adopt AI and ML, but if they can afford not to.

Want to learn more about AI credit risk management? Contact Avenga, your comprehensive AI partner for credit risk.

Your business results matter

Achieve them with minimized risk through our bespoke innovation capabilities. Fill in the form below.