Finding the right patients for the right treatment with AI

Explore the many high-impact applications of AI for greater efficiency in patient recruitment. This is an overview of recent developments in the field.

There is much more to insurance than the traditional risk-based approach. In a nutshell, neoteric insurtech strategies can pave the way for technological disruptions that have never been seen before in the industry.

In a hyper-competitive business landscape, insurance businesses face many pressures. They are tasked with delivering results quickly and they must innovate at an accelerated pace. According to Future Market Insights, the insurtech market is projected to experience a compound annual growth rate (CAGR) of 25.9% between 2023 and 2032. Additionally, insurance businesses face the constant demand of offering better customer service and this massive rise is what drives high competition. In this day and age, insurance companies don’t really have a choice and must improve their operational efficiency if they want to survive and thrive, and technological innovation and disruption is one of the best ways to do that.

Insurance providers have to stay watchful and comply with continuously changing regulations in order to keep up risk prevention and decrease operational uncertainties. On top of that, they have to ensure speedy time to market while outperforming their competition and employing top talent. And, in the current ever-changing business environment, it is essential for insurance companies to align their entire business with IT.

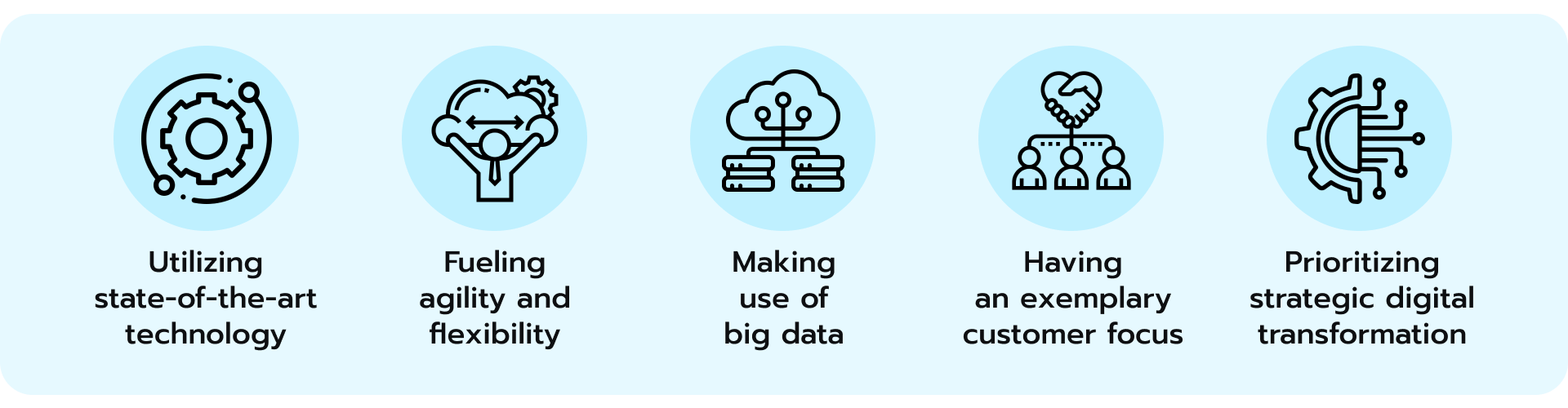

In this article, we will cover five practical elements with examples of how you can take customer data and transform your insurance business with the help of technology. The components we’ll focus on are the following:

Technology brings to the table some very useful tools for many insurtech companies and startups that promote growth and development, and that fosters an information exchange between internal and external stakeholders. It makes tasks easier to do and strengthens the insurtech infrastructure.

Accenture’s Technology Vision 2022 report indicates that insurance customer needs are highly involved, which drives InsurTech companies to seek advancements, innovation, and adoption of new technologies. From Artificial Intelligence (AI) to Metaverse, insurance businesses are on the constant lookout for any way to gain a competitive edge through new technological tools on the market.

New technologies, such as distributed ledgers, AI, Augmented Reality (AR) & Virtual Reality (VR), and quantum computing, are kick-starting the insurance industry’s progress and providing outstanding business opportunities. For example:

As the insurance industry navigates the digital era, the embracement of emerging technologies serves as a key enabler for growth and competitiveness in this highly regulated industry. InsurTech companies are capitalizing on AI, distributed ledgers, AR & VR, and quantum technology so as to enhance their customer experience, streamline processes, and make data-driven decisions.

With the help of technology and smart contracts, the insurance business can:

The strategic application of technology and smart contracts provides the insurance industry with a transformative toolset for boosting performance, customer engagement, security, and competitive standing while streamlining processes and fostering innovative development.

A UK-based insurance startup, Tractable, utilized AI to quicken accident and other fraud prevention, detection, and disaster recovery by using computer vision that reproduces the visual damage evaluation instead of humans conducting the assessments. It closed $119 million of Series D in 7-round funding in March 2021.

With the help of AI algorithms, Tractable can assess vehicle damage in just a few minutes and speed up claim settlements. AI helps to evaluate risk and then reveals any possible inaccuracies that may lead to fraudulent claims and substantial cost savings.

What is more, this insurtech startup claims that the AI algorithms sped up their claims processing process as well as their appraisal procedures by processing photos of areas affected by natural disasters, like hurricanes, and predicting the costs needed for repairs.

Multinational insurance firms like Ageas, Covea, and Tokio Marine are making use of Tractable’s platform so they can deliver the next wave of tech innovation to accident and disaster recovery victims worldwide, and make data-driven decisions that significantly refine the customer experience.

Nowadays, insurtech firms have an essential strategic need for agility and flexibility in their organization, so they can promptly react and adjust to the expanding insurance requirements, and thus provide an overarching value in every area of the business.

Flexibility is an absolutely indispensable component of agility. The old methods and processes were not built for the speed and scale that we see taking place now. A let’s-wait-and-see-how-it-goes attitude is destructive in the long term as competitors are maturing and improving every day.

An agile approach allows insurance organizations to adopt a flexible iterative approach and shift their technological capabilities towards adapting to the quickly changing client needs. Being agile has a well-recognized impact on the insurance industry: it speeds up product delivery from 200% to 400%, decreases development costs from 200% to 300%, and achieves 90% employee engagement.

Many smaller insurtech firms and startups are adapting to their client’s demands and expectations faster than the large players. An agile transformation across an insurance enterprise offers advantages from an iterative approach and cross‑functional collaboration to embracing the entire potential of technology.

Agile processes in the insurance sector harness change. By reorganizing itself in order to meet the needs of the market, an insurance firm can:

Many insurance firms have invested in building agile teams and they work according to the Scrum methodology, but have not made the fundamental change of front‑to‑back work delivery across their enterprise and IT environments.

In a fully agile enterprise, all business operations are immersed in the continuous cyclical process of discovery, prioritization, building, operating, analyzing, and evaluating.

Common roadblocks to the agile transformation of insurtech companies are the following:

To build an effective agile claims management process, an insurance company should use the following tactics:

The agility in insurance processes is instrumental in enhancing market responsiveness, team synchronization, and overall operational efficiency. Overcoming common roadblocks, such as a lack of coordination, synchronization, automation, and committed leadership, is key to leveraging the benefits of agility and ensuring a successful transformation in the insurtech landscape.

The big giants understand this need and are making acquisitions to reinvent the traditional insurance industry arena into what we see now. For instance, in January 2020, Amazon, J.P. Morgan, and Berkshire Hathaway announced that they were teaming up to resolve rising healthcare costs and are planning to revamp the insurance industry. They rolled out their venture, called Haven, to 30,000 employees in the US. With Haven, employees don’t need to pay deductibles. Instead, they can earn money each month by fulfilling specific wellness activities, like keeping their blood pressure below a certain target. The money they earn can be used to cover a visit to a doctor or the cost of medications.

Established processes and structures in large insurance companies are not that easy to change. Slow and manual processes, an outdated IT infrastructure, and reluctant customer services can make an insurance business stagnate.

Not surprisingly, 89% of companies perceive big data as a revolutionary step toward digital transformation. Big data helps insurtech firms to:

In the face of persistent challenges, such as outdated infrastructure and slow processes, insurance companies are recognizing the revolutionary impact of big data in driving digital transformation, enabling deeper customer insights, improving real-time decision-making, and the discovery of new revenue streams and product offerings.

World-class insurance firms utilize the benefits of business intelligence (BI), advanced analytics, and big data in real-time, unlike in the past when it took several days or weeks to obtain data points to compile a report. Insurtech companies can access customers’ behaviors, sentiments, and engagement in order to forecast future customer behavior and analyze movable assets, as well as enumerate business transactions without unneeded third-party approvals.

Incorporating BI and advanced analytics into your processes will improve your business performance and operating costs, and build a competitive advantage.

Learn how we adopted business intelligence (BI) to boost a client’s internal cooperation. Success story

Here’s where new players come onto the stage. They are revolutionizing the insurtech space and designing data-driven experiences. WeFox Group, a German insurtech startup, has grown its revenues to over $100 million and serves more than 500,000 customers, which makes WeFox Group a leading insurtech solutions provider in Europe. The WeFox Group has several insurance brands, of which one of them is One Insurance which increased its revenues tenfold in one year.

One is Germany’s quickest-growing provider of third-party liability and household insurance. The competitive advantage One has is in its ability to make use of big data and understand risk in a much more technology-driven way. It uses predictive risk insurance and geotriggering so that insurees can build short-term insurance around their life. It also allows insurees to both assess the risks and rewards of their injury insurance and create custom insurance packages.

Present-day insurance customers have high expectations of insurtech providers. According to Accenture’s Global Consumer Pulse research, only 29% of insurance customers are happy with their current insurance providers, and as few as 16% are going to buy more from them.

According to McKinsey’s research, the five key factors driving customer satisfaction are:

It may be surprising to find out that ‘settlements paid’ ranks in 12th place, while the insurer’s knowledge, professionalism, etiquette, and politeness are much more important. In other words, the users care more about the service than about getting paid.

An exemplary insurance technology provider will utilize digital innovation to obtain insights, offer personalized services and scale, and profoundly collaborate and connect with its customers. It will excel at delivering a tailored customer experience to their various segments and will build trust within its brand. Insurtech providers that take the initiative to provide their clients with a wider range of high-quality products and services are better positioned to obtain a leading role in the industry.

Therefore, insurance companies that exploit the full capabilities of digital transformation and adapt to the needs of current and potential customers are likely to have the advantage and win the customer’s heart and business.

A great example of a digital-first insurance company is Lemonade Insurance. It’s clearly outperforming its competitors and has invented a new insurance business model based upon behavioral economics, technology, and digitalization. The main value proposition is “instant everything,” with 90 seconds to get insured and 3 minutes to get paid. With this simple offering, Lemonade quickly won customer loyalty by providing a personalized approach and being very easy to use.

Lemonade uses AI and chatbots to allocate insurance policies. It allows its users to file claims on their desktop and mobile (via Lemonade’s iOS and Android apps) without engaging with insurance brokers. Corporate social responsibility is another feature of Lemonade’s business model, as a part of its profits goes to nonprofits of the customers’ choice in Lemonade’s annual “Giveback” program.

As we venture further into the digital era, the importance of a comprehensive and modern approach to insurtech strategy cannot be overstated. State-of-the-art technology, agility and flexibility, big data utilization, and an exemplary customer focus are the four previously identified key elements that shape this strategic approach. Now, however, it’s high time to turn our attention to the 5th crucial element: prioritizing strategic digital transformation.

In an increasingly connected world, digital transformation is more than just a buzzword — it’s a necessity for the survival and profitable growth of any business. For insurance companies, a strategic approach to digital transformation can redefine how they interact with customers and also streamline internal processes, which can ultimately lead to improved customer experience and operational efficiency. This step can be crucial in establishing a competitive edge in a rapidly evolving industry.

Let’s consider the example of Allstate, one of the largest insurance providers in the U.S., which has made significant strides in their digital transformation. They developed an AI-driven tool called “Virtual Assist,” which allows body shops to interact in real-time with Allstate’s remote estimators, speeding up the assessment and repair process for customers.

Furthermore, Allstate employs predictive modeling and Machine Learning in its underwriting and risk assessment processes. Their “Drivewise” telematics program collects data about policyholders’ engaged customers’ driving habits, allowing them to predict risk more accurately and provide personalized pricing models.

The company’s efforts to utilize these technologies have greatly enhanced the customer experience and operational efficiency of the current insurance model, thereby illustrating the transformative potential of AI and Machine Learning in the insurance industry.

Technology has substantially changed the insurance industry. It is an unstoppable process. Auto insurance and insurtech businesses are embracing it by implementing innovative digital technologies and models to make the insurance processes easier and to provide a seamless digital experience to their customers.

These five components of technological disruption, with all the given examples from the insurance industry, are not new. However, the successful implementation of digital technologies is crucial to matching the speed of insurance firms’ actions to the speed of business opportunities. These actions are not trivial because they can improve business performance and customers’ lives, and ultimately disrupt how we measure our milestones.

By reorganizing your mindset to manifest agility and flexibility, and also by implementing AI, big data, and AR & VR in your insurance company, you can get on the path towards sustainable and persistent growth and development. Contact us to get an in-depth understanding of how digital transformation in the insurance industry can help your business grow.

Explore the many high-impact applications of AI for greater efficiency in patient recruitment. This is an overview of recent developments in the field.

Explore essential applications of data and analytics in insurance. Learn how industry leaders use advanced analytics and generative AI for their competitiveness.

Discover how Artificial Intelligence (AI) and Machine Learning (ML) are changing the code of credit risk management in banking.

Dive into the evolving world of Big Data with our introductory article. Explore current trends and future forecasts in Big Data.

Here, we discuss the current AI use cases popular among the biggest industry names and share some AI implementation tips for automotive organizations.

Dive into the insurance industry’s future with our comprehensive guide on the top 10 technology trends for 2024.

Explore our whitepaper to discover what generative AI brings to the table in specific subfields of life sciences and how companies embed digital and AI into their competitive advantage.

Learn how insurance marketing can be elevated through the use of advanced AI technologies.

Start a conversation

We’d like to hear from you. Use the contact form below and we’ll get back to you shortly.